|

|

Posted By Kaylyn Zielinski,

Monday, June 29, 2020

|

By: Josh Johanningmeier | IIAW General Counsel

On May 21, 2020, in Emer’s Camper Corral v. Alderman, the Wisconsin Supreme Court issued a 6-1 majority opinion confirming a rigorous causation standard for negligent procurement E&O claims. The Court ultimately found that, in order to prevail on a claim for negligent procurement of an insurance policy, an insured must show that the promised policy was commercially available to them. While this decision is undoubtedly a win for agents, it is critical that you take care when communicating with clients.

The Emer’s Camper Corral Case and Decision

Since 2004, Rhonda Emer and her husband have sold new and used camper trailers under the trade name Camper Corral. Not long after founding the business, the Emers began purchasing Camper Corral’s insurance through the defendant insurance agency. Starting in 2007, General Casualty Company of Wisconsin insured Camper Corral. However, before the commencement of the 2012-13 policy year, General Casualty sent Camper Corral a nonrenewal notice after two consecutive years with at least $100,000 in hail damage claims.

Following the nonrenewal, the Emers worked with their agent to obtain insurance through Western Heritage Insurance Company. The 2012-13 policy had a $5,000 deductible for hail damage per camper. However, the agent told the Emers that, if they could go claim free for two years, he may be able to negotiate the hail damage deductible down to $1,000 per camper. After two claim free years, the agent contacted the Emers with the news that he had obtained a policy from Western Heritage with a $1,000 deductible per camper for hail damage and a $5,000 aggregate deductible limit. In reality, the Western Heritage policy the Emers ultimately purchased had a $5,000 deductible per camper for hail damage with no aggregate deductible limit.

In September of 2014, another hail storm swept over the Camper Corral lot. This storm damaged 25 of the campers in the Emers’ inventory. Because of the actual terms of the Western Heritage policy, the Emers’ deductible amounted to $125,000. As a result, the Emers sued the agent for negligence, suggesting he had breached his duty to them by failing to adequately describe the terms of the Western Heritage policy. For damages, the Emers asked for $120,000, i.e., the difference between their deductible and the $5,000 aggregate deductible they were promised.

The case ultimately went to trial. However, before the jury could deliberate, the agent moved for a directed verdict, arguing the Emers had not satisfied their evidentiary burden. The trial court agreed, ruling that, without evidence that the policy promised to the Emers was commercially available to them (and not just generally available in the marketplace), they could not prevail on their negligence claim. The Wisconsin Court of Appeals affirmed the trial court, and the Emers appealed the case to the Wisconsin Supreme Court.

According to the State Supreme Court, to prevail on their negligence claim against the agent, the Emers needed to prove four well-settled elements: “(1) [the agent’s] duty of care to Camper Corral; (2) [the agent’s] breach of that duty; (3) injury caused by [the agent’s] breach; and (4) actual loss or damage resulting from the injury.” However, the only issue left for the Supreme Court to decide was the third: causation.

The Wisconsin Supreme Court ultimately held that the Emers had not provided sufficient evidence to satisfy the causation standard. In their arguments before the Wisconsin Supreme Court, the Emers suggested they only needed to prove that a policy like the one they were promised was commercially available. The Supreme Court, though, found that was one step short. Not only did the Emers have to prove that the relevant policy was available in the marketplace, but they also had to show that the policy was commercially available to their business. Put differently, “[w]hether the unavailability is general, or instead particular to Camper Corral, the policy’s unavailability exists independently of any negligence on behalf of the broker.” Thus, as the Emers did not show that the policy promised to them by the agent was commercially available to their business, the Supreme Court affirmed the trial court’s directed verdict in the agent’s favor.

Now What?

This decision is a big win for both insurance agents and E&O carriers defending claims under Wisconsin law. With the additional burden of having to prove specific availability in negligent procurement cases, agents will see fewer judgments against them and, as a result, fewer lawsuits brought in the first place. Further, only one Justice dissented in the Camper Corral case. Thus, even as the makeup of the Court shifts slightly over the next few months, this decision is likely to remain binding precedent well into the future.

With this in mind, you should still see this case as a cautionary tale. Sure, the case ended with a positive result for both the defendant agent, the E&O carrier and insurance agencies around Wisconsin. But, it took a full trial and appeals all the way to Wisconsin’s highest court to achieve that result. It is essential that you take great care when marketing policies to your clients. Doing so will likely save you the hassle of expensive litigation.

Conclusion

Ultimately, the Wisconsin Supreme Court’s decision in Emer’s Camper Corral v. Alderman is a huge win for insurance agents and E&O carriers around the state. This will undoubtedly result in fewer negligent procurement cases brought against agents and stronger defenses in some of the cases and claims that are brought by disappointed insureds. We will keep an eye on the application of this stringent causation standard—it may well cross Wisconsin’s borders into other states.

Tags:

government affairs

insuring Wisconsin

wisconsin independent insurance association

wisconsin insurance agency help

wisconsin insurance blog

wisconsin supreme court

Permalink

| Comments (0)

|

|

|

Posted By IIAW Staff,

Tuesday, June 16, 2020

Updated: Tuesday, June 9, 2020

|

By: Donna Asta | Vice President and Claims Expert Swiss Re Corporate Solutions

It shouldn’t be news to anyone that technological advancements are shaping the world around us. But because new technology changes the way we live, work and play, independent agents need to keep up to date.

Here are a three ways technological trends are impacting personal lines coverage:

Cyber threats. From instant application approvals to auto-renewals, the use of technology is changing the insurance industry. With this changing environment come additional risks and new coverages, such as cyber or data breach coverage.

Your clients use technology to make their lives easier, but it also puts them at greater risk of a cyberattack. Victims may find that they downloaded a document that contained ransomware that disabled their computer system, while others may unknowingly find themselves sent to a phishing website. Damages from these types of attacks can cost thousands of dollars. Are your clients covered for such perils?

Also, in the event of a cyberattack, do your customers have adequate coverage and limits? Personal cyber coverage is becoming more

common. But as it grows in popularity, it is also becoming common for cyber coverage to be excluded from standard homeowners policy and only available by endorsement or a standalone policy. Do the standard homeowners policies you write provide cyber coverage? If not, did you offer it?

Teleworking: Another technological trend is telecommuting, which has become the standard operating mode for at least 50% of the U.S.

population, according to Forbes. However, traditional homeowners policies contain broad exclusions for home business pursuits.

Coverage for personal liability arising out of business pursuits is typically excluded, which prompts the question: Is your customer covered for business performed at home? Agencies should determine whether they have clients who telework or run businesses from home and offer endorsements to existing homeowners and renters policies to cover these pursuits.

The gig economy: There are more than 1 million ride-share drivers working for companies like Uber and Lyft in the U.S. Meanwhile, HomeAway offers 2 million global home listings and Airbnb offers 500,000 in the U.S. alone. Other examples of the gig economy include ad hoc food delivery, package delivery and manual laborers.

Do you know whether your clients are participating in the gig economy? If so, are they covered for property damage, personal liability, injuries requiring health care and loss of income? Agents should start asking these questions before a claim comes in.

Recognizing and reacting to these trends will prepare you to satisfy your duties as a 21st-century personal lines agent or broker. Importantly, staying ahead of the curve when it comes to technology leads to better agency achievement, and higher client satisfaction and retention.

Donna Asta is a vice president and claims expert with Swiss Re Corporate Solutions and is associated with the Chicago office.

This article is intended to be used for general informational purposes only and is not to be relied upon or used for any particular purpose. Swiss Re shall not be held responsible in any way for, and specifically disclaims any liability arising out of or in any way connected to, reliance on or use of any of the information contained or referenced in this article.

The information contained or referenced in this article is not intended to constitute and should not be considered legal, accounting or professional advice, nor shall it serve as a substitute for the recipient obtaining such advice.

Tags:

insuring wisconsin

personal lines coverage

technology

wisconsin independent agent

wisconsin insurance

wisconsin insurance agency help

wisconsin insurance blog

Permalink

| Comments (0)

|

|

|

Posted By IIAW Staff,

Monday, June 15, 2020

Updated: Tuesday, June 9, 2020

|

By: Roger Sitkins | Chief Executive Officer, Sitkins Group, Inc.

One of the best questions I ever heard came from Andy Stanley, the founder and pastor of North Point Ministries in Atlanta: “What will your story be when it’s time for your story to be told?”

Whenever I’ve asked this question at our senior leadership programs or producer programs, it tends to spur considerable thought. I can see that people are asking themselves, “When the time comes, what is my story going to be?” I think this question applies to you regardless of your role in the agency, whether you’re a leader, a producer, or any other team member.

Although we may not be aware of it, we all are creating stories that someday will be told. Perhaps a better word is “legacy.” What legacy are you going to leave? As I’ve said before, eventually everybody leaves their business.

Granted, most of my readers will be in this business for another 10, 15, or 20 years, if not longer. Why? Because it’s a great business that’s creating opportunities and freedoms that most can only dream of. To seize these opportunities and freedoms, however, you must act! As I’m sure you’ve heard me say in the past, “If you’re going to put the time in anyway, you might as well be great at it.”

So here’s another question: If your agency could talk, what would it say? What would it say today, and what would you like it to say five years from now?

Before you answer that, let me share with you the story of a Best Version Possible (BVP) Agency as it unfolds in my perfect world. It starts with asking “What’s it all about in your agency today?”

The 3 Cs

This is how the BVP Agency responds:

Here at the BVP Agency, we embrace several key themes, the first of which is The 3 Cs:Clarity, Consistency, and Commitment.

Clarity means having a clear view of our vision. It’s what we want and why we want it, based on our understanding of the vision’s purpose and value. In terms of Key Performance Indicators, our agency and all of our team know exactly where we are today, where we want to go over the next three years, and exactly how we are going to get there.

We know the resources and tools we need. We know the personal development plans for each team member. And we know our agreed-upon behaviors and strategies.

We’re all on the same page concerning our business plan. In case you’re wondering how it’s possible for everyone to be on the same page, it’s because our business plan is on one page. Unlike most agencies, we have a single-page summary of our Strategic Business Plan that everyone can rally around.

Further, we believe that direction and destination must match up. Because we have absolute clarity on our desired destination, we have to keep checking to make sure our current direction matches that desired destination. Just like an airplane or a ship at sea, if we get off track just a little bit and “stay the course” without recalibrating, we’ll miss our target by a lot.

Consistency is all about our team members never deviating from our “agency’s way of doing business,” which is quite specific. We have

documented processes and procedures that explain with absolute clarity (there’s that word again!) how things are done in our agency. We know our new business processes in all departments. We know our continuation processes in all departments. (As you know, we don’t renew accounts, we continue relationships.) We know how claims will be handled. We know how all day-to-day transactions will be handled. We know how our technology and automation systems apply to our jobs and how to maximize them.

In all areas, we have identified best practices, which are mutually agreed upon and followed. There is absolute buy-in from all team members. We

accomplish this by asking team members for their input before making any improvements (which is an ongoing process). We know that if they’re

part of the design, they’ll buy in more quickly and enthusiastically.

Commitment holds it all together and starts at the top with our leaders, who are committed to our plans. They’re also committed to continual and never-ending improvement because in our agency, good is never good enough. Our leaders are committed to “over-communication,” which, by the way, can never happen. Most agencies under-communicate, but have you ever seen an agency that communicates too much? (You haven’t, because it doesn’t exist!) Our leaders and our team are committed to our Clients, Colleagues, Carriers, and Communities.

The 4 Cs

We want our Clients to have the absolute best experience that creates raving fans who buy all of their insurance and risk management needs

from our agency. These clients would never think of leaving us, and they love sending us referrals and introductions.

Next, our leaders are committed to all of our Colleagues, our team members. They want to attract and retain the very best. They provide

personal development opportunities for everyone. They truly do provide a “Best Places to Work” atmosphere. It feels like family, because it is!

Further, we’re committed to seeking out the best assortment of Carriers to represent. We want deep partnerships, which is why we don’t represent every carrier out there. We know the 80/20 Rule applies to our carriers, and we believe that less is more. We also are committed to crevice marketing, so we represent carriers that let us specialize, thereby

enabling us to go “narrow and deep” in our marketing.

Our final commitment is to our Communities. They are critically important to us! We live here and work here. We realize how blessed we are, and we want to give back. Although we don’t assist/contribute to 100% of the projects out there, we have a Community Service Committee that helps us identify and select opportunities to support and the ways that we can give back. We’re proud to say that more than 75% of our team members have contributed, whether through time or money, to the community projects we’ve chosen.

Our agency’s overall theme is truly to be our Best Version Possible. It’s a constant work in progress. We’ve simply never allowed “good” to be good enough. And while we’re respectful of our competitors, we believe we’ve become the “category of one” in our marketplace, emerging as the agency that has transcended commoditization and that defies comparison.

We simply don’t want commodity-based clients. If price is the only reason someone comes to us, it will also be the reason they leave us. We’ve raised the bar on everything we do. We’re risk advisors who provide solutions well beyond the simple placement and purchase of insurance products.

We are the feared competition, the point of comparison against which all other agencies are measured.

If your agency could talk, how would it compare to the BVP agency described above, and how do you want it to compare five years from now?

Your BVP is out there waiting for you to arrive. Are you ready for the journey?

The author

Roger Sitkins, chief executive officer of Sitkins Group, Inc., is the nation’s number-one “Agency Results Coach.” He established The Sitkins Network™, a territory-exclusive network of high-performing agencies, and The Better Way Agency, a web-based training program that shows agency owners ways to make significant improvements in all areas of the agency. To learn more, please visit www.sitkins.com.

Tags:

Agency Operations

carriers

customer service

insuring wisconsin

wisconsin insurance agency help

wisconsin insurance blog

Permalink

| Comments (0)

|

|

|

Posted By Kaylyn Zielinski,

Wednesday, June 10, 2020

|

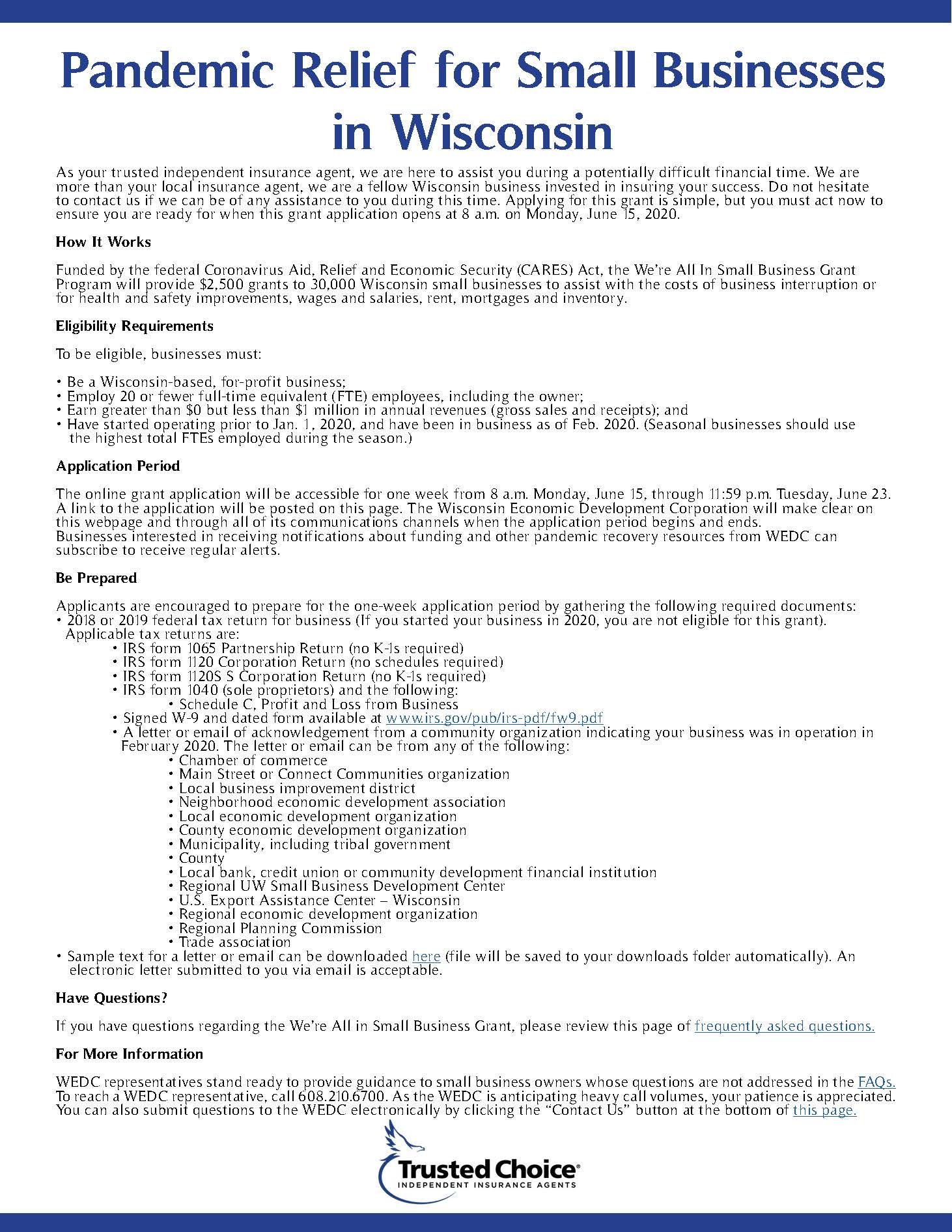

Receiving $2,500 has never been so easy! The IIAW can help!

Funded by the federal Coronavirus Aid, Relief, and Economic Security (CARES) Act, WEDC’s We’re All In Small Business Grant aims to assist with the costs of business interruption or for health and safety improvements, wages and salaries, rent, mortgages and inventory. Grants in the amount of $2,500 will be distributed on a fist come first serve basis to the first 30,000 Wisconsin small businesses that are approved. The online grant application will be accessible for one week from 8 a.m. Monday, June 15, through 11:59 p.m. Sunday, June 21.Just follow the simple 4 step process below to get started. These instructions are also attached to this email.

For more information on WEDC’s We’re ALL in Small Business Grant, click HERE!

STEP 1: DETERMINE ELGIBILITY

To be eligible for the We’re All In Small Business Grant, applicants must meet the following criteria:

- The business is Wisconsin-based and for profit;

- The business employs 20 or fewer full-time equivalent (FTE) employees, including the owner;

- The business has greater than $0 but less than $1 million in annual revenues (gross sales and receipts); and

- The business started operating prior to Jan. 1, 2020, and was operating in February, 2020.

STEP 2: PREPARE

Applicants are encouraged to prepare for the one-week application period by gathering the required documents:

· 2018 or 2019 federal tax return for business (If you started your business in 2020, you are not eligible for this grant).

· Signed W-9 and dated form available at www.irs.gov/pub/irs-pdf/fw9.pdf

· A letter (from IIAW) indicating your business was in operation in February 2020.

According to WEDC, the IIAW is listed as a qualified community organization who can provide you with a letter of acknowledgement that your agency was in business during the prescribed period. We have taken the liberty to prepare this letter in advance to assist you with your application. Attached to this email is the letter you can use to when submitting your application. If you require any assistance, please do not hesitate to contact me directly. It pays to be a member in the IIAW.

STEP 3: APPLY

The online grant application will be accessible for one week from 8 a.m. Monday, June 15, through 11:59 p.m. Sunday, June 21. A link to the application will be posted at wedc.org/WAI-Small-Business-Grant. Don’t forget to gather the necessary information listed above to apply.

STEP 4: PROVIDE GRANT INFORMATION FLYER TO QUALIFYING SMALL BUSINESS CLIENTS

Please don't hesitate to contact anyone at the IIAW if we can be of any additional assistance. It pays (literally) to be a member in the IIAW! See below for a flyer you can send to your qualifying small business clients to help them apply for the grant. Feel free to customize it by inserting your logo, or by contacting kaylyn@iiaw.com to add your logo to the document.

Click here to download the PDF.

Tags:

COVID-19 funds

grant

insuring Wisconsin

pandemic relief

WEDC

wisconsin insurance agency help

wisconsin insurance blog

Permalink

| Comments (0)

|

|

|

Posted By IIAW Staff,

Tuesday, June 9, 2020

|

By: Josh Johanningmeier | IIAW General Counsel

Not since the Thrilla in Manila has a third bout been as eagerly anticipated as the upcoming United States Supreme Court hearing of the latest challenge to Obamacare. Well, perhaps comparing the case to the 1975 finale of the Ali - Frazier rivalry is unfair (to Ali and Frazier), but the case does merit attention. Earlier this month, the Supreme Court agreed to again hear a case concerning the validity of the Affordable Care Act (“ACA”), President Obama’s signature healthcare legislation. If the Court takes this opportunity to overturn the law, the provision of health insurance in this country could fundamentally change. This change would be especially impactful for your business clients.

Case Background

In 2017, congressional Republicans began their efforts to repeal and replace the ACA. When those efforts failed, Republicans changed tactics and instead, chipped away at one of the act’s most well-known, and unpopular, provisions: the individual mandate. To be clear, Congress did not eliminate the individual mandate itself, but, rather, eliminated the tax penalty for failing to acquire health insurance. President Trump quickly signed this change into law.

Seeing an opportunity, a group of 20 states brought suit in the United States District Court for the Northern District of Texas, arguing that the entire ACA is invalid because of the changes to the law. In a previous challenge, the Supreme Court upheld the individual mandate as an exercise of Congress’ taxing power. The states challenging the ACA asserted that, with no tax penalty for violations, the individual mandate can no longer fall under Congress’ taxation powers and must be considered unconstitutional as a violation of individual liberty. Going further, the states argued that the individual mandate is a fundamental component of the ACA, and, as a result, the entire law must be overturned. In a December 2018 decision, District Judge Reed O’Connor agreed and ruled the ACA unconstitutional.

Shortly thereafter, several groups, including Democratic state attorneys general and the House of Representatives, under Democratic control at that point, appealed the decision to the Fifth Circuit Court of Appeals. Given a choice between finding the individual mandate constitutional and overturning the entire law, the Fifth Circuit chose a middle way. The court agreed with Judge O’Connor that the individual mandate is unconstitutional, but sent the case back to the lower court to reconsider if such a holding renders the entire act invalid. The House and the states led by Democratic attorneys general appealed that the decision to the United States Supreme Court, which agreed to hear the case. Based on standard timeframes, the Court will likely issue a decision in spring or summer of 2021.

Now What?

Importantly, it is not clear how the Supreme Court will rule on this case. The ACA has come before the Court on two previous occasions, and it has upheld the law both times. While the makeup of the Court has changed significantly in recent years, all five Justices making up the majority in both decisions remain on the Court. However, the law has now changed, and in ways relevant to the Court’s previous opinions. The takeaway: while it is entirely possible the law will be upheld, you and your agencies should be prepared for it to be overturned.

If the entire law is invalidated, a key impact will be the elimination of the “employer mandate.” As you are likely aware, currently, employers with 50 or more full-time employees, or full-time equivalents, must provide health insurance to 95% of those

full-time employees and their children that is both affordable and ensures minimum value. Coverage is considered “affordable” if employee contributions do not exceed a specified percentage of that employee’s household income (9.78% in 2020). A plan provides “minimum value” if it pays for at least 60% of covered services (including deductibles, copays and coinsurance). If employers violate their mandate, they face a monetary penalty.

If the ACA is overturned, however, there will be of course no employer mandate. This will likely result in many of your business clients evaluating changes to their employee health plans. It is critical that you and your agencies work with legal counsel so that you can make informed decisions when it comes time to design plans responsive to your clients’ needs.

Conclusion

While it is unclear if the Supreme Court will take this opportunity to overturn the ACA, it is crucial to be prepared in the event that it does. Keep an eye on this column and other IIAW publications for developments on this case, and make sure to work with legal counsel to ensure that you and your agencies are able to successfully navigate what could be a complex path forward.

Tags:

affordable care act

commentary from counsel

insurance general counsel

wisconsin insurance blog

wisconsin supreme court

Permalink

| Comments (0)

|

|

|

Posted By IIAW Staff,

Tuesday, June 9, 2020

|

By: Misha Lee | IIAW Lobbyist

On May 13, 2020, the Wisconsin Supreme Court declared the state’s Safer-at-Home order unlawful, invalid, and unenforceable. When the ruling was first announced, businesses faced some uncertainty as to how to operate. However, it now appears there are no statewide requirements governing their operations.

By a 4-3 decision the court limited Evers’s ability to make statewide rules during emergencies such as a global pandemic, instead requiring him to work with the state legislature on how the state should handle the outbreak.

The justices wrote that the court was not challenging the Governor’s power to declare emergencies, “but in the case of a pandemic, which lasts month after month, the Governor cannot rely on emergency powers indefinitely.” Notably, the court allowed Emergency Order #28 to remain valid as to school closings for the

2019-2020 school year, which means that while businesses may open, schools remain closed.

Neither the Governor nor the legislature have yet to offer replacement guidance on COVID-19 suppression measures. A scope statement for emergency rule-making was recently withdrawn by the Department of Health Services (DHS) for lack of legislative support. Many businesses have voluntarily adopted standards which require physical distancing, capacity limits or call for face coverings. However, there are no statewide

requirement to do so. Each business is left to determine for themselves what measures, if any, they wish to put in place.

Immediately following the ruling, a few Wisconsin counties and municipalities (i.e.

Milwaukee, Madison, Dane County, Brown County, Kenosha County) instituted their own local orders. However, some of those have since been lifted out of concern for a lawsuit or have expired, including those effecting most of the Milwaukee suburbs. Notably, Dane County and the Cities of Milwaukee and Madison continue to have versions of a Safer-At-Home order still in place.

As businesses around the state gradually begin to open up, there is concern about exposure to lawsuits that may be brought by employees or customers that contract the virus. A group of businesses trade organizations with the Wisconsin Civil Justice Council (WCJC) have been working on a legislative proposal that would provide civil immunity for businesses that reopen during the COVID-19 pandemic. Such a proposal requires legislative approval and signature from the Governor and the timeline is uncertain if and when such a measure would pass.

Tags:

governor evers

insurance in wisconsin

insurance lobbyist

safer-at-home order

wisconsin

wisconsin insurance blog

wisconsin supreme court

Permalink

| Comments (0)

|

|

|

Posted By IIAW Staff,

Tuesday, June 9, 2020

|

States have gone to war against some municipalities over COVID-19. Executive orders currently in place in many states still bar certain businesses considered “non-essential” from opening; but some municipalities have told their respective governors they are opening the community regardless.

Governors finding themselves in these situations have undertaken various tactics to prevent these municipalities from carrying through with their reopening plans. North Carolina’s governor told a county that all state funding would be cut if they opened, the county capitulated. Other governors, seemingly out of options, have undertaken a unique and indirect tactic – misrepresenting insurance coverage.

Although this sounds like an odd tactic, the goal is to scare the business owners into remaining closed. If the governors can successfully dissuade the business owners, it doesn’t matter what the city or county does, businesses won’t open solely out of fear.

Governors and their representatives are publicly stating that if a business opens in violation of the executive order, doing so places its insurance coverage in jeopardy because of the “illegal,” “criminal” and/or “dishonest” acts exclusions. The problem is, there is enough untruth in these statements to make them lies.

Let’s review the truth or half-truths of these claims on a coverage-by-coverage basis. Note, the following analysis is of unendorsed policy language, endorsements can alter application of this policy language analysis.

Commercial General Liability (ISO’s CG 00 01 04 13)

Coverage A – Bodily Injury and Property Damage Liability.

Simply, there is NO illegal or criminal acts exclusion applicable to Coverage Part A. One state knowingly took indecent liberties with the “Expected or Intended Injury” exclusion in its attempt to assert that coverage would be denied.

The expected or intended injury exclusion does not act to deny claims resulting from opening against a governor’s orders. This exclusion applies to the actions of an insured that one would EXPECT or INTEND to cause injury such as punching someone in the nose or setting a trap. A reasonable person intends and would expect that someone would be injured by such acts.

There does not appear to be an applicable exclusion in Coverage Part A. So, a slip-and-fall incident is covered, a products liability claim is covered, basically anything covered under Coverage A in “normal” times is covered if/when the business opens – even against a governor’s orders.

Coverage B – Personal and Advertising Injury Liability.

There is a “Criminal Acts” exclusion appliable to personal and advertising injury coverage. Within Coverage B the specific exclusion reads:

2. Exclusions:

This insurance does not apply to:

d. Criminal Acts

“Personal and advertising injury” arising out of a criminal act committed by or at the direction of the insured.

“Personal and advertising injury” is a defined term. Basically, this exclusion applies to activities and actions such as libel, slander, defamation of character, violating a right of privacy, wrongful eviction, false arrest and other such actions. If any of the acts listed in the definition is done in violation of a law, there is no coverage.

If the store owner calls the governor a nasty name, that would be excluded; but only if doing so is considered a criminal act. Thus, this exclusion is a non-issue.

Coverage C - Medical Payments.

In short, there are no exclusions for “illegal,” “criminal” or “dishonest” acts in Coverage C. Where the insured had coverage before the orders, they still have coverage.

Commercial Property

Within ISO’s CP 00 10 10 12 - Building & Personal Property Coverage Form there is one reference to “illegal.” The policy excludes coverage for “contraband, or property in the course of illegal transportation or trade.” Although this is intended to exclude coverage for products that are illegal to import, export or sell, the wording may present problems if the insured opens against government orders.

Two key questions arise:

• Is operating in defiance of an executive order a criminal act (making it illegal); and

• If it is a criminal act, does ignoring an executive order mean the operation is “in the course of” illegal…trade?

Illegal or Criminal Act

An illegal act is one that is forbidden by law. In the absence of this pandemic, the reasonable assumption is that the insured is a legal operation and was operating legally. Whether an executive order disallowing the operation of a business is given the effect of or is equivalent to a law is a question for the courts.

If operating in defiance of an executive order is forbidden by law (making it a criminal act), will the “law” be upheld in court? Reports are that at least one state court has determined that stay-at-home orders are not legal. Whether other courts will follow this lead is unknown.

For sake of this analysis, let’s make the worst-case assumption that operating in defiance of an executive order is considered a criminal or illegal act. If operating against a lock down order is a criminal act, this is strike one towards the lack of property coverage.

However, given the anecdotal evidence, these orders do not appear to hold status as a law. Governors can make emergency declarations that can be enforced to a certain degree; but if they were, in fact, laws and the actions were illegal, the governors would not need to use scare tactics and/or threats such as the revocation of the business’ operating license, they would simply have the owner arrested.

Additionally, laws cannot generally be created by edict. A law (statute) generally requires approval of both houses. Yes, as stated, an executive does have broad powers during a declared emergency, but that does not include the ability to create a law or statute.

Lastly, in general the US is designed as a “bottom-up” regulatory model. The only reason the NC county succumbed to the governor’s orders was because the state threatened to take away state funds. Evidently, opening is not illegal, it’s just against the governor’s wishes contained in the emergency declaration. (It’s unlikely that any level of government would want the executive to have the ability to create law by edict.)

If the actions are NOT criminal, coverage for the property is NOT excluded.

Is Operating in Defiance of the Order “In the Course of” Illegal Trade

“In the course of” can be defined to mean “during a specified period.” Other definitions include “in the process of,” and “during.”

Black’s Law redirects the definition of “course of trade” to “trade usage.” “Trade usage” redirects to “usage.” Under “usage” is found the meaning of “trade usage.” A long way around to the information needed.

Trade or trade usage in Blacks Law essentially means the common methods of operation. Other sources define trade to mean a business or occupation entered into for profit.

Given the above, it appears any business operating is “in the course of trade.” If operating in defiance of a governor’s order is illegal (a criminal act), the business is “in the course of illegal trade.” Operating in the course of illegal trade negates property coverage during the time of illegal operations.

The commercial property form does not limit the application of this wording to real or personal property – the wording applies to all property.

Unfortunately, there is not a “fix” for this possible exclusion of coverage. The lynchpin or key factor to whether the property is covered or excluded from coverage is whether the operation is illegal. If opening is not illegal, there is coverage; if opening is a crime, there is no property coverage.

ISO’s CP 10 30 09 17 - Causes of Loss - Special Form contains an exclusion for dishonest or criminal acts; however, the wording applies to actions undertaken by the insured to damage or destroy covered property. This exclusionary wording does not apply to the operation of the business within or outside the allowances of an executive order.

Is coverage excluded for property losses when the business is operating in defiance of an executive order? This may ultimately be a question for the courts; but it appears:

If a governor’s decree does NOT carry the weight of a law, it’s unlikely this wording would apply – meaning there would be coverage regardless the governor’s wishes;

If a governor’s decree IS given the weight of a law, making the act of opening illegal, the insured may lose property coverage; or

If a governor’s declaration is granted the weight of a law, but such decree is struck down by the courts, coverage may be reinstated.

From a property coverage perspective, the question of coverage is murky. Carriers may or may not attempt to spit hairs to deny or provide coverage.

Workers’ Compensation and Employers’ Liability

Does NCCI’s workers’ compensation policy respond to cover an injury to an employee arising out of and in the course and scope of employment if the business is operating against that orders of the state? Workers’ compensation is a unique coverage, the policy responds in accordance to the guidelines of the state’s workers’ compensation statutes. To answer the question, the statute must be reviewed. If statute does not exclude protection to employees working in violation of the law, the work comp policy responds and pays for injury – regardless of the executive order.

Because workers’ compensation is for the benefit of the injured worker, it is unlikely any state law would disallow coverage for any work-related injury, even if the business is operating against an executive order. This violates the spirit and intent of the coverage. In fact, some work comp statutes specify that it applies to workers whether lawfully or unlawfully employed.

The respective state law must be reviewed, but such limitation or exclusion is unlikely to be found. Furthermore, there is no wording in the policy itself that would allow the insurance carrier to seek repayment from the insured. Thus, opening in defiance of an executive order does not appear to jeopardize workers’ compensation coverage.

Part Two – Employers’ Liability does contain exclusionary wording regarding employment in violation of the law. The policy reads:

C. Exclusions

This insurance does not cover:

3. bodily injury to an employee while employed in violation of law with your actual knowledge or the actual knowledge of any of your executive officers.

Is the employment in violation of the law or is the operation in violation of the law? The apparent intent is to exclude employers’ liability protection for those employed in violation of federal guidelines regarding status as a legal worker in the US. Given the intent, this exclusion does not appear to apply. But remember, this is regarding the employers’ liability protection only, this wording does NOT apply to workers’ compensation.

Business Auto (CA 00 01 10 13-Business Auto Coverage Form)

There is no illegal, criminal or dishonest act exclusion in Section II – Covered Autos Liability Coverage of the business auto policy (BAP).

Like the CGL, there is the Expected or Intended Injury exclusion; but, as in the CGL review, this is irrelevant in regard to this conversation.

Operating in disregard to the executive order does not appear to negatively affect the liability coverage provided by the business auto policy. If the BAP did exclude illegal acts, there would be no coverage for injury caused when speeding, when making an illegal turn or many other actions that are illegal.

Neither is there an applicable exclusion under the physical damage coverage. No specific exclusionary wording appears to affect uninsured/underinsured motorist coverage either.

Apparently, the business auto policy responds regardless of any orders in place.

Professional Liability and Errors & Omissions Policies

There is no “standard” professional liability or errors and omissions (E&O) contract, thus each will require separate review. However, most of these forms do contain exclusions related to criminal conduct. But does such wording exclude coverage simply because the business is open regardless of the governor’s declarations?

Given the intent of coverage, professional liability and E&O policies cover the professional activities of the insured and the harm caused by the improper practice of those activities. Opening against the wishes of the governor doesn’t seem to entail the professional activities, it is a business decision.

For example, assume insurance agencies were not considered essential businesses and were forced to close. If an agency owner decided to reopen in spite of the order, any act or failure to act for or on behalf of a client may result in an E&O suit.

IF opening is a criminal act (it’s not clear if such act is criminal), does that activate the criminal acts exclusion?

Opening in defiance of any order has no correlation to the erroneous act of the agent. They are separate and distinct incidents. One has no relationship to the other.

This same logic appears to apply to all other activities covered by either a professional liability or an E&O policy. Opening against the wishes of the governor does not appear to affect coverage.

However, some governors have threatened to revoke and some already have revoked certain professional licenses. If holding a professional license is a condition of the professional liability or E&O coverage, then these coverages appear to be in jeopardy.

Most occupations that require professional liability or E&O coverage also require a license to provide the service (not the same as a business license).

If the government, through its police powers, revokes a professional license, the coverage may cease to exist for any future events. Revoking a professional license is not the same as revoking a business license. For agents, this is revoking the agent’s P&C license, not the agency’s license to exist. Whether such revocation is allowed by law is not a topic for discussion in this article.

Executive or Management Liability

Directors and Officers (D&O), Employment Practices Liability (EPL) and Fiduciary Liability are the three most commonly discussed executive or management liability coverages. Like professional liability and E&O, there are no “standard” forms. Likewise, these forms generally do contain exclusions related to illegal, criminal, and/or dishonest acts.

Following are examples from two separate management liability forms:

Exclusions:

The Insurer shall not be liable to make any payment for Loss in connection with

any Claim made against any Insured:

A. alleging, arising out of, based upon or attributable to:

(2) the deliberately fraudulent or criminal acts of an Insured; provided, however, this exclusion shall only apply when it is finally adjudicated that such conduct occurred;

Exclusions:

We will not pay for any “loss” resulting from any “claim”:

A. Based upon, attributable to, or arising

in fact out of any dishonest,

malicious, fraudulent or deliberately

criminal act or any willful violation of

any statute or regulation;

Notice the key words common to both exclusionary examples, “based upon,” “attributable to” and “arising out of.” Neither exclusion applies to any management liability suit unrelated to opening against the will of the governor. The only suits that might be excluded are management liability suits directly related to the violation of the decree; otherwise, the policy is unaffected.

Findings

Overall, opening in defiance of a governor’s decree appears to have little effect on insurance coverage. Questions arise in two policy types:

Commercial property; and Professional liability / E&O policies.

If, and this seems to be a big “if,” the act of opening is a criminal act, the insured’s commercial property coverage may be compromised. And if the state revokes the business owner’s professional license (not business license), the professional liability or E&O policy may exclude coverage.

The fear tactics being used by some states surrounding insurance coverage are largely unsupported. Not being lawyers, no agent should advise on what constitutes a criminal act, but agents can and are within their licensure to explain insurance language.

Tags:

illegal acts exclusions

insurance policy

virtual university

wisconsin insurance blog

Permalink

| Comments (0)

|

|

|

Posted By IIAW Staff,

Thursday, June 4, 2020

|

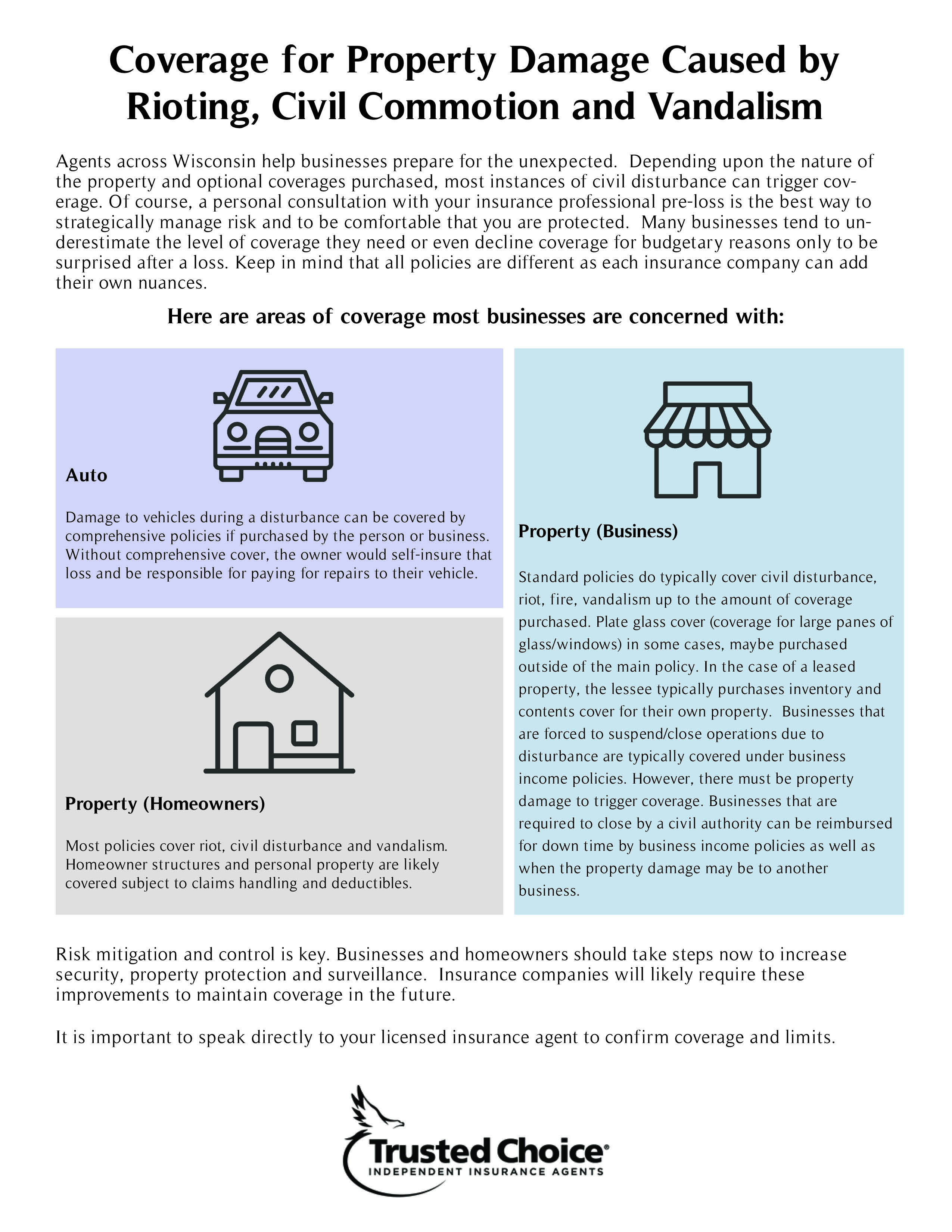

Agents across Wisconsin help businesses prepare for the unexpected. Depending upon the nature of the property and optional coverages purchased, most instances of civil disturbance can trigger coverage. Of course, a personal consultation with your Insurance professional pre-loss is the best way to strategically manage risk and to be comfortable that you are protected. Many businesses tend to underestimate the level of coverage they need or even decline coverage for budgetary reasons only to be surprised after a loss. Keep in mind that all policies are different as each insurance company can add their own nuances.

Click here to access the full document. Email kaylyn@iiaw.com to customize this document with your logo for your agency's use.

Tags:

civil disturbance

insurance claims

riots

risk mitigation

vandalism

Permalink

| Comments (0)

|

|

|

Posted By Kaylyn Zielinski,

Wednesday, June 3, 2020

Updated: Thursday, May 21, 2020

|

COVID-19 has changed the agent’s errors and omissions (E&O) landscape for the next several months. While we can’t predict the number of agents who may have E&O claims at this point, the odds are high that if you don’t get sued, an agent you know will.

Proper actions and reactions when threatened or served with an E&O suit arising out of this pandemic are of utmost importance. Once a threat is made or a suit filed, the allegedly improper act or omission has already occurred - don’t worsen the situation by making bad decisions. Remember these “dos” and “don’ts” if you find yourself in an E&O situation.

Let’s start with the first MAJOR don’t: Do not overreact to the claim. Understand that there is no shame in being accused of an error or omission, especially given the weird aspects of this COVID-19 situation. Even the best practices and procedures may not protect the agency right now. Anger, either toward yourself or others, is counterproductive and serves only to increase the weight of the situation.

Do Not Do These Things

Do not, under any circumstances, alter the client’s

file. What’s done is done. Making changes creates the appearance that there is something to hide. Accept what is there and prepare for what comes next.

Do not discuss the claim with anyone other than the claims representative, defense attorney or any other member of the office directly involved in the claim. The only individuals who need to be involved in any discussion related to any E&O claim are those personnel directly related to the care of the plaintiff’s account and those defending the agency.

Do not make any admission of liability or wrongdoing; and do not offer or make payment.

Do not provide any written or recorded statement to the plaintiff without your E&O carrier’s claim representative present.

Do not allow inspection, copying or removal of client files and records without consulting with your E&O claim representative.

Do not try to manage the claim on your own. The E&O carrier has more experience and is better able to manage the process. Allow those with more experience and resources to manage the suit.

What to DO

What should your immediate and ongoing “do’s” be following an E&O claim?

Notify the E&O carrier of a “claim” or potential claim immediately. Provisions in the E&O policy require the insured to notify the insurance carrier as soon as practicable following the receipt of a “claim” or any indication of a potential claim.

Listen for “trigger” words or questions. Some words, phrases or questions just don’t seem normal, in fact, they sound like something a lawyer would say. If your client uses terms like “duty,” “breach” or “breach of duty,” assume they have been talking with a lawyer. Also pay attention to the questions that are asked, does it seem like they are trying to trap you into admitting something? Notify the carrier of a potential claim if words or phrases seem to indicate a lawyer is already involved.

Assume every conversation is being recorded. Regardless of the legalities of recording a conversation, assume your answers are being recorded. Pick responses carefully.

Gather and organize all pertinent records related to the insured and the situation. But when doing this, remember the second “don’t” - don’t alter them. The claim representative needs all the information to conduct an investigation and prepare and provide a proper defense.

Write down all the information known about the incident surrounding the claim. Each member of the team directly related to the client and the incident giving rise to the E&O claim should record all they can remember about the incident or incidents on which the claim is based. This should be a factual narrative statement in chronological order. Leave out opinion and emotion. This is the time to act like you are talking with Joe Friday from Dragnet – just the facts. Who, what, when, where and why is all that should be contained in these accounts.

Assign one person as the claim leader. One person should be assigned the duty to report, track and manage all COVID-19 E&O claims within the agency.

Cooperate with the E&O carrier. This includes providing information and facts that look bad for the agency. Hiding or hedging certain aspects of the facts surrounding the situation on which the claim is based creates distrust between you and your insurer; it also makes the agency look guilty. The insurer is on your side.

Make sure you comply with all policy conditions and requirements. If the agency fails to comply with all E&O policy conditions, coverage may be jeopardized.

Hopefully, You Will be Spared

Hopefully, you and your agency will not need this information. If not, that’s great. But given the uncertainty of this current situation, it’s better to be prepared.

Tags:

coronavirus

COVID-19

errors and omissions

Permalink

| Comments (0)

|

|

|

Posted By IIAW Staff,

Monday, June 1, 2020

|

By: Bernard Rosauer, President of Wisconsin Compensation Rating Bureau

By this time many of us have attended national webinars, read national periodicals containing articles regarding Covid-19 and the exposure it may bring to the workers’ compensation industry.

Logic 101 teaches us a basic flaw in logic is the hasty generalization. The problem with consuming national information and applying it to one state is obvious. In addition, early to market national predictions based on inadequate data often wastes time and miss the mark… by a lot.

In some cases, particularly in specific states where laws are changed or enacted quickly , generalizations regarding the specific state are reasonable and necessary. Otherwise, unless each state is looked at with a critical eye and a gathering of state specific data, reports with a wide span are less useful if not misleading when applied to one state.

Here’s Wisconsin specific information you can rely on.

Wisconsin Specific Workers Compensation Impact of Covid-19

Wisconsin Compensation Rating Bureaus transition from office to home.

Your Bureau’s transition was seamless. There was no change in service availability and work was processed on time despite the many Covid-19 related phone calls that added to our workload.

As president of the organization, I am proud of the entire staff, the flexibility and extra hours worked to ensure availability, and timely decision-making for

members, employers, agents and all other stakeholders. Our Rating Committee, Governing Board and all employees really did step up and I acknowledge all of them and their communal effort.

Claims Received

The WCRB does not collect real time data regarding claims. Still, we believe it is important to understand, at least anecdotally, what volume and types of Covid-19 claims are being presented by first responders, healthcare workers and other workers deemed essential. A hasty generalization made by using countrywide statistics could have led us in the wrong direction. With national reports predicting up to a 50% decrease in overall claims activity (because of the unemployment plunge) through April 2020, Wisconsin has seen a decrease of approximately 25% in new claims opened.

WCRB is also tracking claims received in the first responder worker categories defined by the statutory changes in Wisconsin Workers Compensation Act that allow presumptive but rebuttable claims be honored by a defined list of first responders and healthcare workers. This will help support estimates for rating purposes at a later date.

At a high level and at this period of time, these Covid-19 exposures are not of such a great volume that an overall impact on rate impact will be great. Of those reported the vast majority, approximately 95%, had treatment consisting of diagnosis then staying home and waiting for the illness to pass.

‘Furloughed but Paid” Workers

With reports of employers paying workers out of goodwill while those workers were furloughed, something needed to be done to remove the payroll for ‘Furloughed but Paid’ workers from eventually being used in rating the risk.

Wisconsin became the first state in the country to construct a filing with rules that granted employers relief knowing that they would not be charged a rate for their goodwill. The Bureau developed unit statistical code 0012 which was approved by Wisconsin’s OCI in less than a week (that sounds easier than it was.) NCCI and other rating bureaus subsequently changed their filings to include 0012 or another code that enabled employers to place payroll for workers who are not working and not apply a rate toward that payroll.

Covid-19 and Worker’s Compensation in Wisconsin Updates and FAQ’s

For a full list of FAQ’s regarding Covid-19 in Wisconsin, visit www.WCRB.org and look for the ‘Click Here’ link for Covid-19 Updates and FAQ’s.

Here are some of the MOST frequently asked questions:

Who is considered a paid furloughed employee for WI worker’s compensation insurance purposes?

By definition, a paid furloughed employee is one who is still being paid where they have been given a temporary layoff, an involuntary leave or another modification of normal working hours for a specified duration. This is for payments made by the employer during the paid furloughed time under the Governmental Emergency Order regardless of when it was earned.

(It is important to understand that Paid Furloughed Workers code 0012 can only be used when absolutely no work is being performed for the employer. In addition, it imperative that the employer keep clear and irrefutable records when reporting employees as paid while on furlough.)

What if Code 0012 is used fraudulently by an employer to falsely lower WC premiums?

Code 0012 can ONLY be used if an emergency order is issued by a governmental official. Code 0012 is defined as: Paid Furloughed Workers During A Governmental Emergency Order Impacting Employment. If a governmental emergency order is not in effect, code 0012 cannot be used. During a declared government emergency order, improper use of this code or the use of false or misleading documentation in support of

reallocation of payroll to this code is a violation of the law and may subject the employer/owners to fines, penalties and/or imprisonment for fraud.

If a paid furloughed employee continues to be paid by their employer, is their payroll excluded from the employer’s worker’s compensation insurance

premium?

If an employer continues to pay furloughed employees their normal wages and the employer keeps separate, accurate and verifiable records, the payroll will not be included for the basis of premium.

How is the payroll to be split when an employee works part of a day and is furloughed part of the day?

If the employee is performing work duties for any portion of the day, no division of payroll is acceptable.

Will COVID-19 claims be included in my future experience rating modifications?

Wisconsin procedures will be consistent with those previously applied to other Extraordinary Loss Event catastrophe codes. Valid claims coded with catastrophe code 12 and reported to Wisconsin will be excluded from experience rating calculations for any employer(s) incurring one or more such claims.

Tags:

COVID-19

payroll

workers' compensation

Permalink

| Comments (0)

|

|